The decentralized finance landscape has long been plagued by a fundamental paradox: while the promise of permissionless yields attracts billions in capital, the structural volatility of those yields drives institutional and risk-averse liquidity away. For years, DeFi participants have been forced to ride the chaotic waves of fluctuating Annual Percentage Yields (APYs), unable to secure the predictable forecasting models that define traditional finance (TradFi).

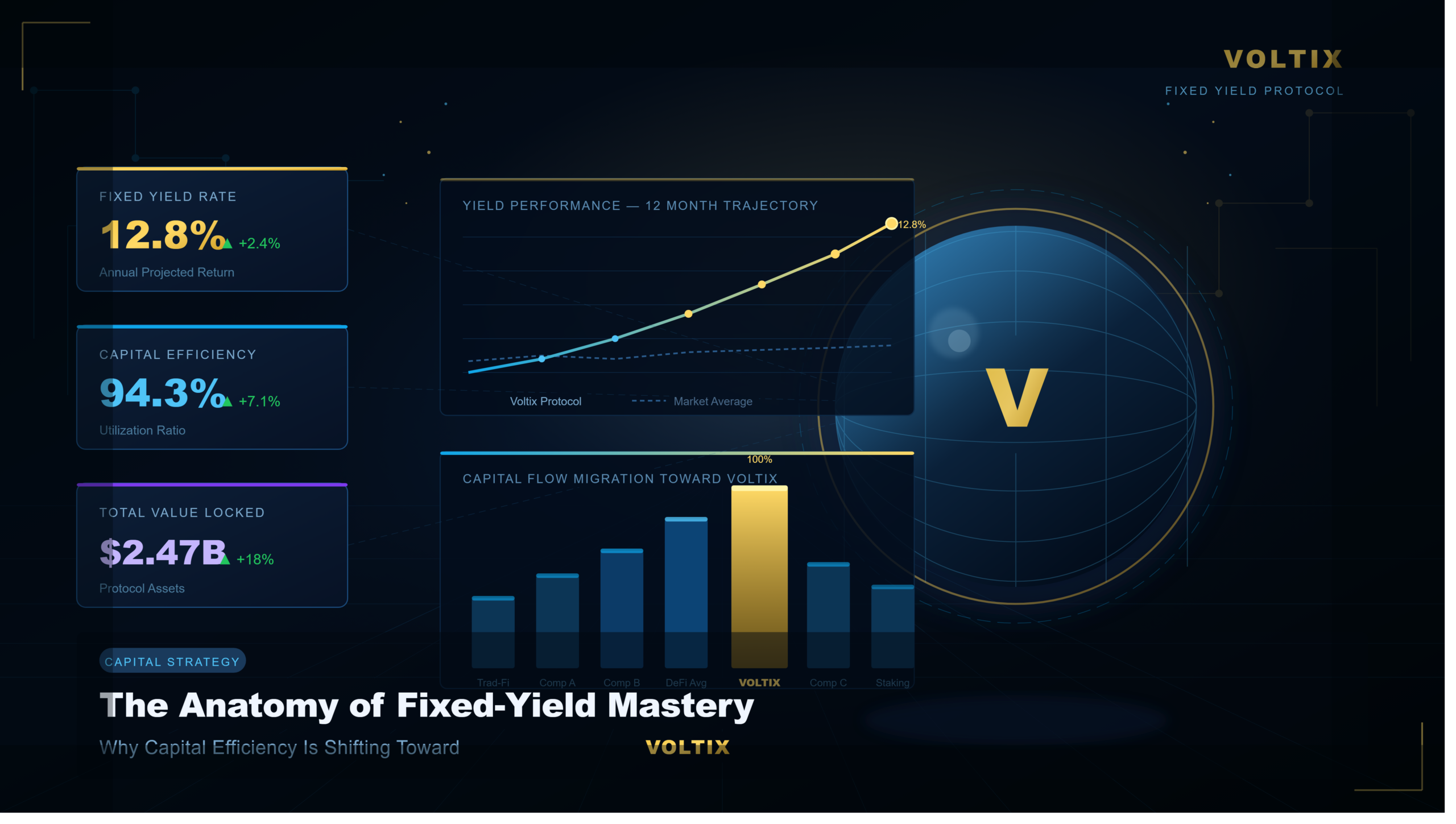

Enter Voltix. By engineered design, this protocol aims to dismantle the unpredictability of decentralized yield markets, offering a sophisticated framework for interest rate swaps, fixed-rate lending, and leveraged yield trading.

To truly understand how Voltix modifies capital efficiency, we must move past basic marketing speak and dissect the core mechanics of its AMM structure, its margin engines, and the exact strategic plays that sophisticated market participants are deploying to hedge risk or amplify returns.

1. Decoding Search Intent: What the Market Demands to Know

Before unpacking the architecture of Voltix, it is critical to address the specific information gaps that exist among current market participants:

-

The Primary Intent: Advanced DeFi users and institutional liquidity providers want to know exactly how Voltix secures predictable fixed yields without creating systemic insolvency risk.

-

The Secondary Intent: Yield farmers and algorithmic traders want to understand how to leverage the protocol’s margin engine to speculate on interest rate fluctuations with minimal capital upfront.

-

The Common Confusion: Many mistake fixed-yield protocols for simple lending pools (like Aave or Compound). Voltix operates on an entirely different layer—decoupling the underlying principal asset from its fluctuating interest rate component.

2. The Core Architecture: How Voltix Engineering Operates

At its absolute foundational level, Voltix functions as a specialized Automated Market Maker (AMM) tailored for Interest Rate Swaps (IRS). In traditional markets, interest rate swaps represent a multi-trillion-dollar sector where institutions trade variable-rate cash flows for fixed-rate cash flows. Voltix ports this exact institutional primitive on-chain but optimizes it for the hyper-fluid dynamics of crypto assets.

The Decoupling Mechanism

When capital enters a standard yield-bearing pool (such as stETH, cUSDC, or a Rocket Pool derivative), it generates a variable rate of return. Voltix splits this position into two distinct functional components:

-

The Fixed-Rate Seeker (The Hedger): A user who wants to lock in a guaranteed APY for a set duration. They deposit capital, agree to a fixed rate, and pass their variable upside to the counterparties.

-

The Variable-Rate Seeker (The Speculator): A trader who believes the underlying pool’s APY will skyrocket past current market expectations. By taking the variable side, they collect the fluctuating yield of the fixed-rate seekers, often using massive leverage to multiply their gains.

The Virtual Liquidity Model

Unlike traditional AMMs (like Uniswap V2) where liquidity is evenly distributed from zero to infinity, Voltix utilizes a concentrated, virtual liquidity framework engineered specifically for yield rates. Since interest rates for blue-chip assets typically fluctuate within a predictable historical band (e.g., 2% to 12%), liquidity providers (LPs) can concentrate their capital strictly within these bounds. This results in unprecedented capital efficiency, allowing massive trade volumes to occur with minimal price slippage.

3. Advanced Trading Strategies: Hedging and Speculation

To extract real value from Voltix, market participants must look beyond passive holding. The protocol unlocks three definitive archetypes of advanced yield management.

Strategy A: The Institutional Macro Hedge

Imagine an asset manager holding $10 million in a variable-rate stablecoin pool. Current yields sit at 6%, but macro indicators suggest market activity is cooling, which will inevitably drag the APY down to 2%.

-

The Execution: The manager deposits the portfolio’s yield profile into Voltix, purchasing a Fixed-Rate Swap.

-

The Outcome: For the next 90 days, the manager locks in a guaranteed 5.5% APY. Even if the broader DeFi market dips to a 1.5% average yield, the portfolio achieves its target metrics, maintaining predictable treasury growth regardless of market downturns.

Strategy B: The Leveraged Yield Long (The Speculator’s Play)

Conversely, suppose a network upgrade or a sudden spike in leverage demand across DeFi is imminent. You predict that liquid staking derivatives (LSDs) like stETH will see their variable yields spike from 4% to 8%.

-

The Execution: Instead of buying stETH outright—which requires substantial capital—you open a Variable-Rate position on Voltix using 10x leverage.

-

The Outcome: Because you only need to post enough margin to cover potential rate movements rather than the underlying principal asset, a small upward shift in the market APY generates exponential returns on your deposited collateral. If the rate moves up by 2%, your 10x leveraged position captures a 20% return relative to your margin.

Strategy C: Delta-Neutral Yield Arbitrage

Sophisticated quantitative traders continuously monitor the spread between different yield generation platforms and the fixed rates offered on Voltix.

| Source Platform | Native Variable APY | Voltix Fixed Rate | Arbitrage Action | Risk Profile |

| Liquid Staking (ETH) | 4.8% | 3.5% | Short Variable / Long Fixed | Delta-Neutral; execution risk |

| Stablecoin Pool | 8.2% | 9.1% | Long Variable / Short Fixed | Low-risk if liquidity remains high |

| Layer-2 Yield Pool | 14.5% | 11.2% | Lock Fixed via Hedging | Smart contract dependency risk |

4. The Margin Engine and Risk Management Realities

While the concept of leveraged interest rate swaps is highly attractive, it introduces a unique set of structural risks that users must comprehend. Voltix uses a sophisticated dynamic margin engine to preserve system solvency.

Liquidations Without Principal Loss

In a typical crypto lending protocol, getting liquidated means your underlying asset (like WBTC or ETH) is sold off to cover your debt. On Voltix, liquidations operate differently because you are trading rates, not the spot token.

If a variable trader utilizes extreme leverage and interest rates move aggressively in the opposite direction of their bet, their margin account dips below the maintenance threshold. The margin engine will auto-liquidate the position, but the risk is strictly isolated to the margin posted for the interest rate derivative—not the broader, uncommitted principal assets.

Impermanent Loss in Yield Space

For Liquidity Providers, concentrated liquidity comes with a variation of impermanent loss known as Rate Impermanent Loss. If interest rates shift violently outside of the price range an LP has specified, their pool liquidity converts entirely into one side of the trade (either all fixed or all variable cash flows). LPs must actively manage their ranges or utilize automated vault managers to avoid becoming stuck in underperforming rate brackets.

5. Common Misconceptions in Interest Rate Trading

Misconception 1: “Fixed Yield Means Zero Risk”

A fixed yield guarantees that the rate of return will not fluctuate based on market demand. However, it does not erase structural risks. Smart contract vulnerabilities, oracle failures, and systemic decoupling of the underlying wrapper asset (e.g., a liquid staking token de-pegging from its base asset) remain present risk vectors.

Misconception 2: “Voltix Requires You to Lock Up Your Crypto Forever”

Many users assume that entering a 180-day fixed yield pool means their assets are completely inaccessible for six months. In reality, because the positions are tokenized or managed via dynamic AMM pools, positions can typically be exited early by executing an offsetting swap—though this may incur a minor cost depending on how market rates have shifted since entry.

6. Blueprint for Execution: Step-by-Step Onboarding

For teams or individuals looking to integrate Voltix into their current asset management workflow, follow this deployment matrix:

Step 1: Capital Assessment and Target Selection

Determine your baseline objective. Are you trying to protect an existing yield portfolio from falling rates, or are you looking to speculate on upcoming network congestion? Identify the asset pool (e.g., stablecoins vs. liquid staking assets) that aligns with your thesis.

Step 2: Analyze the Rate Spread

Evaluate the current Fixed Rate vs. Underlying Variable Rate. If the variable rate is significantly higher than the fixed rate, the market is pricing in a future decline in yields. If the fixed rate carries a premium, the market expects yields to surge.

Step 3: Margin Allocation and Leverage Calculation

If opting for a variable strategy, calculate your liquidation price relative to historical interest rate floors and ceilings.

Ensure your margin buffer can withstand sudden, brief spikes in yield volatility without triggering automated liquidation protocols.

Step 4: Continuous Monitoring

Utilize analytics dashboards to track your position health. Because interest rates react instantly to macroeconomic shifts, on-chain governance changes, and protocol incentives, setting up automated alerting systems for rate deviations is highly recommended.

7. Frequently Asked Questions

What exactly is Voltix?

Voltix is a decentralized interest rate swap protocol that allows DeFi users to trade variable yields for fixed yields, or use leverage to speculate on rate movements within an automated market maker framework.

How does Voltix guarantee a fixed yield?

The fixed yield is not sustained by artificial token emissions. Instead, it is structurally guaranteed by matching users who want a fixed rate with counterparties (or speculators) who are willing to pay a fixed rate in exchange for capturing the fluctuating variable upside of the underlying asset.

What happens if I want to close my fixed position early?

You can exit your position before maturity by executing an inverse swap on the platform. Depending on how current market interest rates compare to the rate you locked in, you will either realize a slight premium or a minor discount upon exit.

Is my principal capital at risk of liquidation?

Only the assets deposited into the margin engine to back your interest rate swaps are subject to liquidation. Your core underlying principal remains separate unless you have actively committed it as margin for a highly leveraged speculative trade.

How do oracles play a role in Voltix?

Voltix relies on secure, low-latency oracles to continuously track the historical and real-time compounding yields of external protocols (such as Aave, Lido, or MakerDAO). This data ensures the AMM accurately prices the swaps relative to actual market performance.

The Horizon of Yield Architecture

The evolution of decentralized finance requires a transition from speculative asset appreciation to structured, predictable cash-flow systems. Protocols like Voltix represent the bridge between these eras. By giving users the granular toolsets required to trade, hedge, and amplify interest rates independently of spot token prices, the ecosystem moves one step closer to displacing traditional fixed-income markets. Whether you utilize it as an insurance policy against dropping yields or an engine for capital-efficient speculation, mastering the mechanics of interest rate swaps is an indispensable skill set for the modern digital asset manager.

Leave a Reply